National Institute on Retirement Security – March 2019 (excerpts reprinted)

by Diane Oakley and Kelly Kenneally

Click here to view the full article

Changes to the U.S. retirement system during the past several decades have put retirement in peril for most working Americans. When all working individuals are considered, the typical American has zero dollars saved for retirement. Among workers who have managed to accumulate savings in a retirement account, that typical account balance is only about $40,000. And even when accounting for an individual’s entire net worth—considered a generous measure of retirement savings—more than three-fourths (77 percent ) of Americans fall short of conservative retirement savings targets for their age and income based on working until age 67.1 This massive retirement savings shortfall can be attributed to a decades-long degradation of our nation’s retirement infrastructure. Most of the workforce lacks an employer sponsored retirement plan, fewer workers have stable and secure defined benefit (DB) pensions, while 401(k)-style defined contribution (DC) individual accounts provide less savings and protections. Also, increases to the Social Security retirement age translate into income cuts for retirees. According to the U.S. Government Accountability Office (GAO), private sector employers since the 1980s have moved

away from offering traditional pensions that provide workers with a guaranteed, monthly income stream that cannot be outlived and offer professional asset management.2

Instead, private sector employers have shifted from pensions to individual accounts like 401(k) plans, if they offer employees any retirement plan at all. With 401(k) plans, the risks and the bulk of the funding burden fall squarely on individual employees, who tend to have difficulty contributing enough on their own to accumulate sufficient savings for retirement. Employees typically also lack the requisite investment expertise, while many also find it challenging once retired to calculate precisely how to spend down their retirement savings in an optimal manner so that

their nest egg lasts as long as they live.3

Meanwhile, retiring Baby Boomers are feeling the financial sting of changes to Social Security implemented in 1983 that

are gradually raising the full retirement age to 67. This means that workers turning 62 in 2019 face increasing reductions in Social Security benefits if they start receiving benefits before their normal retirement age. For example, starting benefits at age 62 results in receiving only 72.5 percent of the full benefit that would be payable at age 66 and a half. If a person born in 1957 waited until reaching age 65, he or she would receive 90 percent of the full benefit. Once fully phased in for Americans born in 1960 and later, the reduction in Social Security benefits for those choosing to draw benefits at age 62 will equal 30 percent less than the benefits at the full retirement age of 67. Despite these benefit cuts, the Social Security program remains in need of a longer-term financial fix. The program has resources to pay scheduled benefits until 2034, but after such time the program will have financing to pay only 79 percent of benefits.4

Against this troubling backdrop, the National Institute on Retirement Security (NIRS) conducted a survey of working age Americans to measure their sentiment on a range of retirement issues.

* * *

Most public employees continue to receive pensions as their primary retirement benefit. In addition to providing retirement

security for workers who often have lower salaries than their private sector counterparts, pensions also serve as a workforce management tool to recruit and retain workers.11 In recent years, public employee pension benefits have remained in the headlines—from articles on teachers striking for better pay and maintaining benefits to news reports about possible legislative changes. At the same time, state and local governments continue to actively enact pension reforms designed to improve funding and recover the deep investment losses that all investors experienced in the years following the 2008 global financial crisis. Since 2009, every state has passed reforms to one or more of its pension plans. The changes took different forms throughout the country—from increasing employee contributions to raising retirement ages.12

Also, ideological organizations opposed to government programs continue to attack public retirement systems at the national and state levels. Some of these organizations are working to switch public employees from pensions to DC accounts even though this wholesale change has proven to raise costs to taxpayers and dramatically worsen public pension funding levels while undermining the public sector work force.13

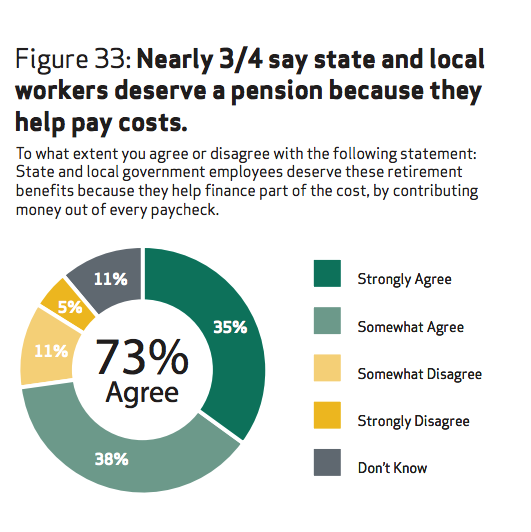

Against this backdrop, Americans were asked their views about public pensions. The data indicate that Americans express strong support for public employee pensions because some public employees have high-risk jobs or lower pay, the funding of the benefits is shared with employees, and pensions help recruit and retain skilled workers. Specifically, nearly three-fourths of Americas say that state and local workers deserve a pension because they help pay for these retirement plans (Figure 33).

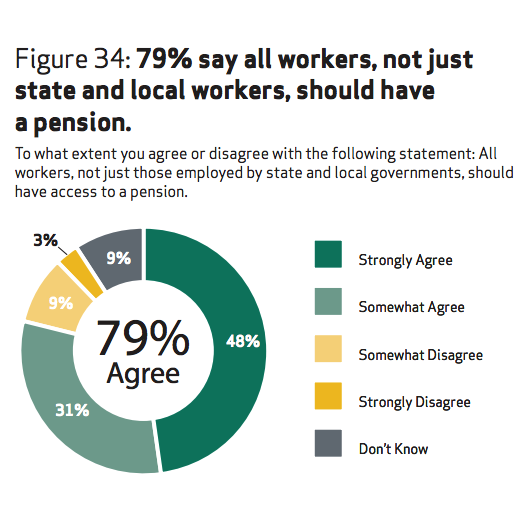

Unlike private sector pensions, public employees make significant contributions to their pensions each pay period, and those employee contributions are rising in many jurisdictions. In fact, the data suggest that Americans do not begrudge public employees for their benefits, but instead would like to receive similar retirement benefits. Some 79 percent say all workers, not just state and local workers, should have a pension (Figure 34).

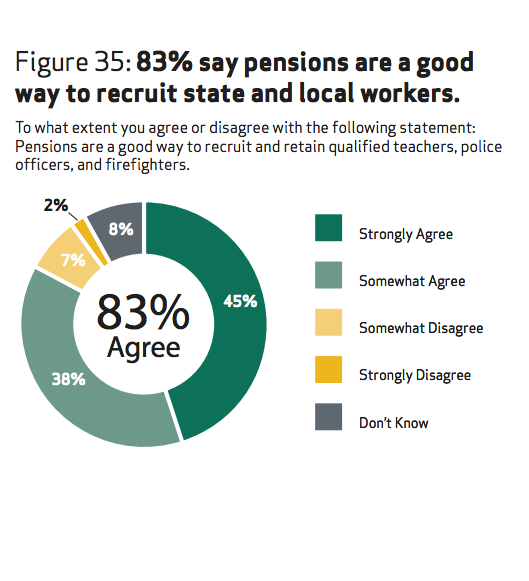

Americans also see the value of pensions beyond providing retirement security. These retirement plans serve as a tool to attract and retain public workers, which is increasingly important in the public sector especially in a tight labor market and when state and local governments continue to face steep recruitment and retention challenges.14 The polling finds that some 83 percent agree that pensions are a good way to recruit and retain state and local workers (Figure 35).

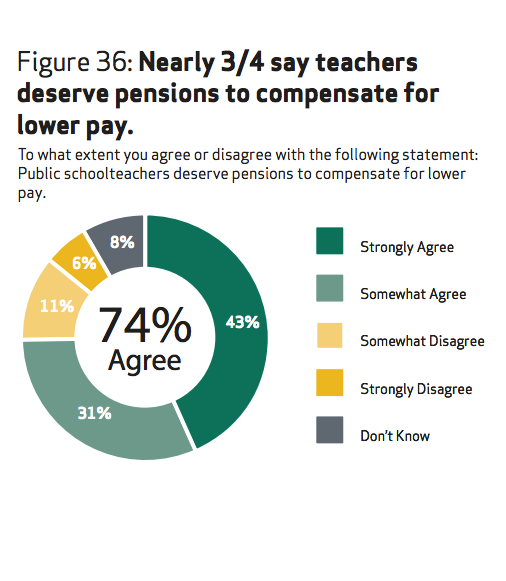

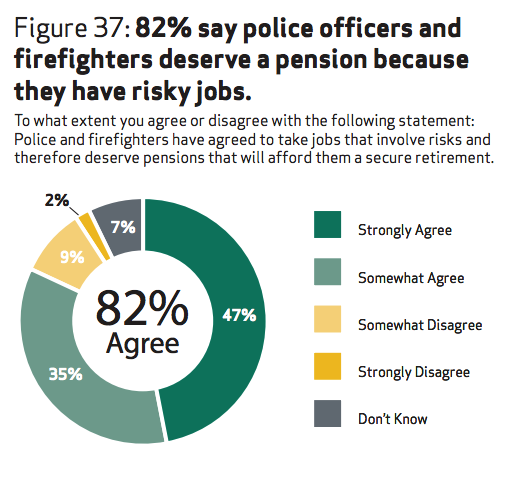

Americans also see the value of providing these retirement benefits to public workers, including teachers, police officers and fire fighters. Nearly three-fourths say teachers deserve pensions to compensate for lower pay at a time when teacher strikes over education funding and pay persist into 2019 (Figure 36). And, an overwhelming majority of those polled (82 percent) say that police officers and fire fighters deserve a pension because they have risky jobs (Figure 37).

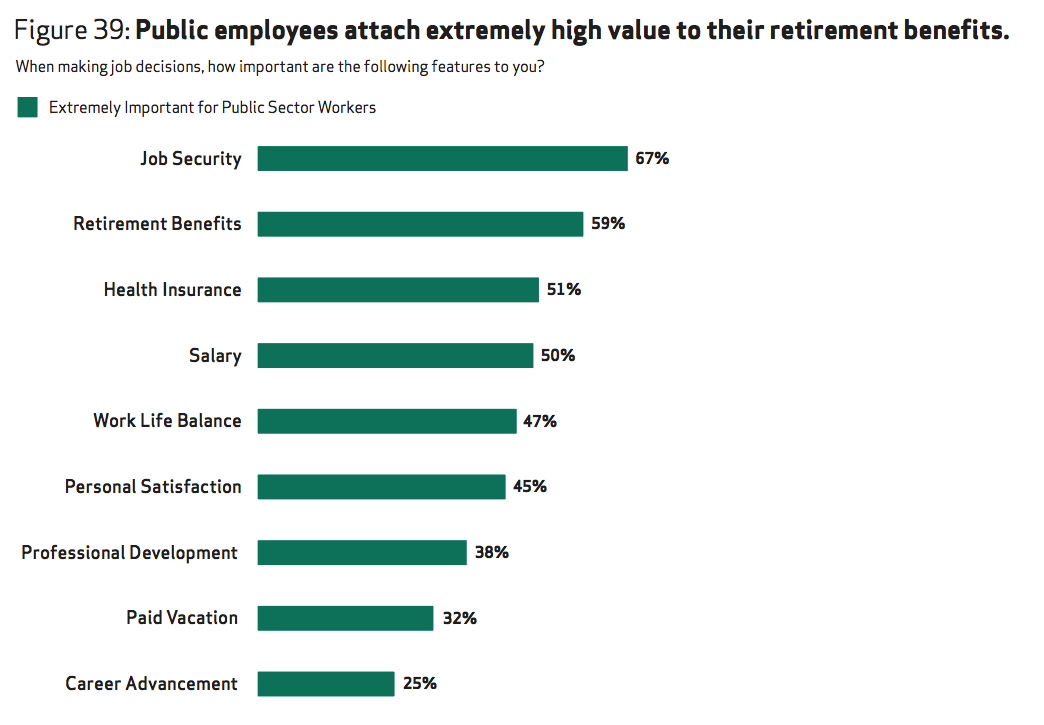

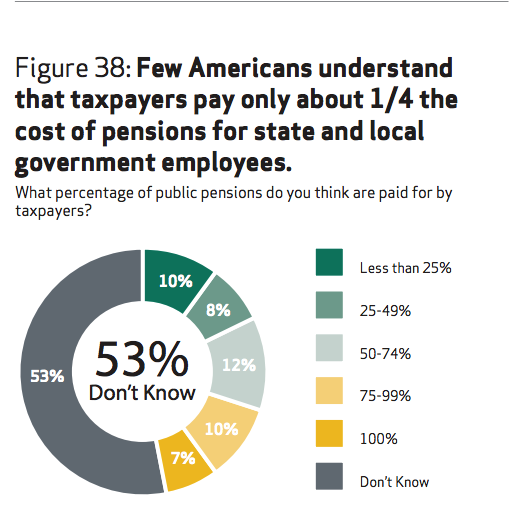

The polling finds that few Americans are aware that taxpayers pay only about one-quarter of the cost of pensions for state and local government employees (Figure 38). Pensions with lifetime retirement income remain prevalent in the public sector, which is not the trend in the private sector that continues to shift employees to individual retirement plans like 401(k) accounts. Interestingly, the results indicate that public sector retirement benefits are extremely important to a majority of public sector workers (59 percent), second only to job security (Figure 39). In contrast, retirement benefits were extremely important to only 41 percent of private sector workers. This high value placed on retirement benefits may indicate that public sector workers are willing to sacrifice salary in exchange for a secure retirement. Salaries for public sector workers lags significantly behind their private sector counterparts.16